Debt is a powerful force that keeps us as slaves. In this episode I will show you an older and better alternative, “Social Credit”, and do my best to explain the difference. For Social Credit is a liberating and useful force in the emerging post-Jump and Networked Social Economy.

How we used to borrow

Traditionally people borrowed money to purchase a “productive asset” such as a tool or against a predictable event such as the harvest. What this means in practice is that traditionally debt was self-liquidating. The productive asset, such as a loom, increased the value of the business and threw off enough cash to pay off the loan. Or the harvest came in and the seed loan was paid off.

This idea of a productive asset included the home. Traditionally, people mainly worked from home. So your house was also a work space and so it was a generator of income. Your lodging was a productive asset.

The big idea here is that we usually only borrowed money to finance a productive and self-liquidating asset. Only in desperation, or if we were an aristocrat, did we borrow money to finance consumption.

How we borrow today

Today, we mainly use debt to finance the consumption of items that lose their value quickly. These include clothes, furnishings and even cars. We even borrow for events, such as meals and vacations, that have no lasting value at all. Central to this now is borrowing for education. A BA in History has no direct connection with paid employment. But a plumber’s ticket does.

With ever increasing debt but no productive assets, we climb onto a treadmill where there is no payoff or release. This is even true for our homes. Today most of us work away from home and so our homes, this definition includes places that we rent, have become a net-cost and so a drain that never goes away. Rent or domestic mortgage payments are amongst our most significant never ending chains of financial obligation.

Using this approach to borrowing, we never escape. So, if you step back and examine how we use debt today, we see that much of it is in our choice. We can choose not to finance mere consumption or things and events that are in themselves transitory.

What we can do is to change our approach to borrowing and return to a more traditional way of seeing the use of debt.

It is hard to do this if you are caught up in the pre-Jump belief system of proving your status by “show.” It is much easier to do this if you no longer are captured by this external vision of your worth as a person.

How banks lend

Bank lending today is also different from how credit was extended in the past. Deep down, lending is an art that is tightly connected to an understanding of both the business involved and the person who is the borrower. But today, lending is based on a set of simplistic algorithms that use the income stream from a job as a proxy for future income. This is why self-employed people have such a hard time.

Banks rely so much now on the algorithms that they no longer have the staff that can use the ancient art of lending. If the old lending was like a French restaurant, the new is like Mcdonalds. If it is not on the menu, it cannot be done.

How history can help us

Social Credit is maybe the second oldest profession. The easiest way to understand its timeless principles is to look back at the country store. In rural communities in North America, cash only entered the local system after harvest. Owners of local stores had to extend credit to the local farmers.

There were two parts to this equation.

Firstly, the store owner had to make a personal assessment of the family and then of the farm itself. All of this was based on the length of time that the store owner knew the person and the place. Here is the “Art” of lending and why true lending is “social”. It is based on relationships that are tangible. Above all, Character is the key component. The decision to lend was more about “would” he pay me back rather than “could” he pay me back.

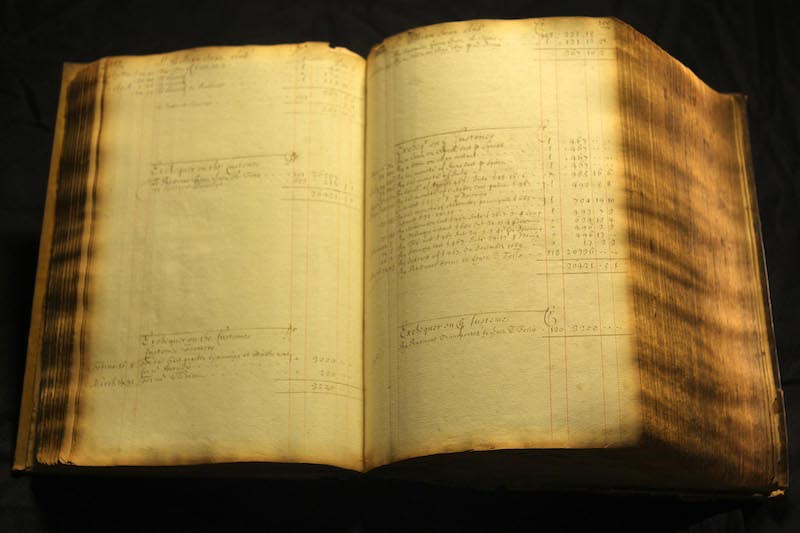

Secondly, the details of the debt were kept in a ledger. The ledger is at the heart of the system. Here are not only records but the ability to move debt around. Each debt is an obligation, based again on the character of the borrower and the quality of the collateral. These obligations can be sold or discounted to others, thus reducing the overall exposure of the store owner.

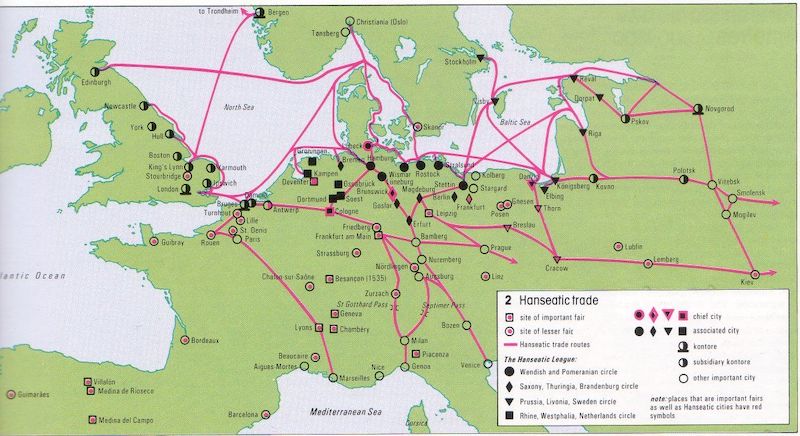

Using a ledger, you can also scale such a system. In the 14th century, we see the apogee of such an idea in the Hanseatic League. Here a series of Baltic towns each had their own ledger and then a master ledger that included all the towns in the league. By using this system, the League could finance a fleet in common and depots such as the depot they had in London. The same principles applied and periodically the system was flushed by cash when a sale was made outside such as to Tudor England.

So here you see the core ideas behind the old system of banking that has existed for all time, until recently. But there is one more aspect that is helpful to understand before we move onto what can we do today.

A major cost in any project is labour. In Amish society, and in many rural communities even today, “barn building” still takes place. Here the principal supplies the materials and the community the labour. Here it is “social credit” that is the system. Here the principle is “Reciprocal Obligation”.

The more that you contribute to your community, the more the community is obliged to help you.

The two systems overlap. For at the heart of both is the character of the “borrower” and the depth of that person’s relationships in their community.

Applying the Model to the Post Jump World

This is a picture of my friend, the late Raymond Loo. Raymond was an organic farmer on PEI who, had a popular stall at the Charlottetown Farmers’ Market. Everyone on PEI that used the market knew and respected him. Raymond was also central to all discussions on PEI that involved the betterment of agriculture. He was a man of character with a vast network of people who loved and trusted him. As you can see, he embodied the core of the old model.

He wanted to expand his operation which meant that he would need to expand his herd of cows, pigs and hens. This would require cash that he did not have or a bank loan. Instead of borrowing from a bank, he went Social. I set up an Indiegogo site for him where we pre-sold the meat in the summer beginning with the chicken, then the pork in the fall and finally with the beef in the winter.

The campaign was of course a huge success. My fee? Chicken, Pork and Beef!

A modern application, Indiegogo, used the principles of old banking. People financed Raymond because they liked and trusted him to deliver and also because they wanted him to be successful.

This model of customers pre-funding their food purchases directly from trusted suppliers is now common in micro agriculture. It is generally known as Community Supported Agriculture or CSA.

While many new farmers sell their food directly at local farmers’ markets or in stores, others have flourished through the increasingly popular system of community-supported agriculture, or C.S.A.

The model sees members directly support a nearby farm by buying a share in the winter, giving farmers a cash infusion to buy seeds and supplies, in exchange for a weekly basket of fresh food during the harvest months.

Codiac Organics Ltd. in Moncton, N.B. has a farm market on site, but also relies on community-supported agriculture.

“It takes a lot of pressure off the farmer,” says Fran Day, who owns and operates the booming urban farm with her husband Mark.

“We get money upfront to buy seeds, and consumers get a regular supply of in-season vegetables.”

Demand for Codiac Organics’ C.S.A. program was so high this year, Day says her farm had a lengthy waitlist.

“Conventional farming numbers are down, and organic farming is going up,” she says. “We see interest growing every year.”

Source here and more on Heart Beet Organics and Amy Smith and Verena Varga.

So is “barn building” where “Wwoofers” work for bed and board to learn and so take the cash out of labour.

The model for “Social Credit”is simple but hard to pull off.

- You borrow only for productive reasons – to finance a farm, a book, a piano for lessons etc

- You have to keep your business small enough to be personal – so that your customers know and care about you and of course trust you

- Your character and so trust is paramount

- The loan is self-liquidated by the delivery of the service/product

Like the Hanseatic League, such a system can be scaled using network principles but the core principles above have to be respected. So Cheeky Creek Farm, a local family farm that raises heritage pigs is extending from its direct relationship with over 600 customers by creating a co-op with several other local farms.

Here they will create, as the Hanseatic League did, a common store and the use of a common butcher. By doing this, they will decrease their distribution costs and increase the quality of their product.

The Future

This ancient model is working well in the new micro-food systems that are growing all over the west.

But the model is not restricted to food producers. All those in the Post Jump world can use it. More here in my short book about this.

In a later post, I will make the case for it being Food Systems that shape our ways of life and culture. In so doing, I offer this idea. That if you want to change the world in a larger sense, then getting behind the new food model is the best way ahead.

Epilogue – Raymond Speaks

Here we have Raymond making his pitch in 2012

3 thoughts on “The Jump # 13 – The Chains of Debt and the Opportunities of Social Credit”